For a New Party of Well-Being, Qualitative Growth and Science and against all exclusivist narratives.

For context see:

1) « Credit without collateral: The unlikely philo-Semite Nietzschean sequel to Bretton Woods.» March 20, 2008

2 ) «The Treasury and the Fed: Epilogue to my earlier essay ”Credit without collateral”», April 1st, 2008

(Freely accessible in the Section International Political Economy of the old experimental site www.la-commune-paraclet.com )

Table of Content:

The evolution of « credit without collateral »

The UK, UE, Spain, and US current strategies.

Swap lines and SDR increases.

Annex: Comment on the FOMC May 4, 2022 meeting.

xxx

The evolution of « credit without collateral »

A new epoch of hegemonic speculation is opening; it is based on a new disconnection between tightening credit conditions and continuous pouring of liquidities from the Central Banks despite earlier hopes to enforce a QT in order to normalise the balance sheets. This is building on top of the existing contradiction which opposes the real economy to the speculative economy. It will be nuanced according to the conditions prevailing within each currency area managed by the neoliberal monetarist dogma but, in the end, it will induce the same contradictions in each of them.

Margin calls are becoming perilous catalysts as the composite inflationary spiral imposes its logic in a blind narrative academic, economic and political environment. CDS valuations are immediately affected by the discrepancy between nominal and real values of assets. This plays out in a context of total financialisation of the economy and of total subservience of fiscal and budgetary policies to the global speculative markets.

To add insult to injury, the leading classes, who are well aware of their inexistent understanding of the inflationary phenomena, are nevertheless sanguine about shifting the cost of fighting CPI inflation on the shoulders of ordinary citizens and workers. Hence, financial assets are automatically indexed while wages are not, except those of the top economic and political brass. This foolish ideological choice adds to the aforementioned discrepancy between nominal and real value.

We are glad to report that former IMF Director M. Jacques de Larosière also made the point about the negative real rates while underlying that high inflation is a tax which hits the less fortunate. With great realism he notes that speculative capital contributes little to productive activities: « Jacques de Larosière : “L’inflation est une taxe qui frappe les plus malheureux !” , Boursorama , https://www.youtube.com/watch?v=_qdQHcHtXyI

The neoconservative neoliberal and monetarist counter-reform launched by Volcker-Reagan in 1979-1982 culminated with the « credit without collateral » financial structure that was ushered with the repeal of the 1933 Glass Steagall Act in 1999. This soon led to the subprime crisis of 2007-2008. In short, the banking prudential ratio was de facto replaced by a permanent bailout in the form of QE and other liquidities, this being added on top of the fiscally deducted debt-provisioning thus transforming the Central Bank in the de facto prudential ratio. This system is now giving way to a new epoch of hegemonic speculative finance, that of « credit without collateral ». It now unfolds in an environment marked by important negative real interest rates which are ideologically, although absurdly, motivated by the need to lower an increasingly inflated CPI, while ignoring imported and organic inflations.

I suppose that the last nail in the « credit without collateral » coffin could be a generalised « people’s QE ». In the Italian context, I have already alerted to the fact that the « politica dei ristori » developed during the Covid self-inflicted crisis was turning permanent. Minimal sustenance for the masses and transhumanist policies seem to be the way toward the long-announced « society of new domesticity and new slavery ».

The capitalist financial system confuses many basic realities and concepts. It does not differentiate between money and credit, instead it amalgamates both into a nonsensical Fisherian « income stream » managed by the presumed universal and perennial « acquisitive mind » according to two investment considerations, namely risk and time. Everyone from the housewife, the househusband, the worker, the lower and upper-middle classes, the CEO and CFO, all are seen as investors who need to manage their « income flow », whatever that is. Learning from Black Friday and the Great Depression, the system used to distinguish between deposit and commercial banks thanks to the Glass Steagall Act of 1933, but this is a thing of the past. Trump even added more water to the already watered down Dodd-Frank. Moscovici et al. followed suit in the Eurozone thus confirming the consolidation of the « credit without collateral » speculative regime.

Whereas classical interest rate is always deducted from profit, the speculative interest rate is legally instituted as a legitimate rate of profit to the detriment of industry and of the real economy in general which it cannibalises with it unsustainable Roe and Ebitda. In fact, the bourgeois paradigm in all its shapes and forms cannot even make the difference between « real economy » and « speculative economy ». The latter is assumed to be transient and thus to lead faster to equilibrium, a notion that is at the center of the « efficient capital » theory; variations are assigned to marginal causes such as bad information and behavioral choices.

This is very problematic. The confusion between money and credit impedes any scientific understanding of the economic sphere and in particular of inflations (in the plural.) The money in circulation should amount to the salary masses, namely the real salary mass which, in an optimal system of full-time full-employment, would be necessary and sufficient to allow all exchanges implied in the reproduction of the economic system, be it stationary equilibrium or dynamic equilibrium. In a full employment setting, salaries by their rotations equal the exchange value of all the Means of production and Means of consumption exchanged during a reproduction cycle to ensure Reproduction. There is no structural inflation (See the Synopsis.) Productivity is the major law of motion of capital; it feeds capitalist competition but, in so doing, it « frees » parts of the labor force thus causing unemployment levels that cannot always be absorbed by new or intermediary sectors. Today both are mainly capital intensive making any inter-sectoral adjustment even more difficult.

Be it as it may, unemployed people – and the non-active labor force in general – must stay alive, hence the question is raised of who takes care of this necessity and how their « livelihood » is ensured. The real salary mass plus this amount going into the sustentation of the inactive labor force constitutes the social salary mass. The ratio of the social salary mass over the real salary mass defines the rate of structural inflation, the only true and direct form of monetary inflation. When the social salary mass is financed organically through social dues levied to finance the 5 branches of Social Security, no structural inflation is induced. However, when the « livelihood » of the inactive labor force is ensured by the printing press, hence on the public debt, structural inflation does appear and soon develops into a spiral. At its height, the European Social State and the Anglo-Saxon Welfare State almost achieved full-time full-employment except for a frictional or seasonal rate of unemployment. In such a setting, with the help of public credit and planning inducing greater macro-economic competitiveness which in turn induces a greater micro-economic productivity that can be shared, it is easy to conceive of recurrent cycles of reduction of working time, be it through the lowering of pension age, the lowering of the work-week or the added work holydays and paid leaves. (See my Tous ensemble)

To structural inflation must be added two other main forms namely imported inflation that could be dealt with through the rate of exchange of the national currency and/or through tariffs, and organic inflation which sends one back to situations in which prices systemically diverge from the underlying exchange value. This is, for instance, the case with today’s imperfect competition induced by the Gafam and the other big transnational firms which can impose their own terms, hence changing the whole structure of relative prices in a given Social Formation.

The banking and financial system gets even more skewed when speculation becomes hegemonic in the sense that the speculative interest rate is now legally treated as a legitimate rate of profit. Then, instead of being deducted from profit as any interest would be, it forces the system to tend toward an average rate of profit through the mobility of capital – which is heightened by the financialisation of the economy and the predominant role of the stock-exchange. This naturally happens to the detriment of industry and indeed of any economic activity necessitating long-term investments.

Moreover the hegemony of speculative finance irremediably invalidates the fractional banking system which is the internal cybernetic control mechanism of capitalism. The other mechanism takes the shape of recurrent crisis known as Business or Trade Cycles which, from time to time, purges the system of its excesses. The so-called « invisible hand » of the market driven by the individual profit motive of the capitalist acquisitive mind induces huge wastes and gross misallocations of resources, thus producing speculative expansions in some sectors that are accompanied by strong contractions in others; recurrent purges are thus inevitable and necessary to rebalance the system. But they are ruled out by the current continuous bailouts. Structural crisis of the Capitalist Mode of Production are instead caused by the introduction and massification of successive waves of technology; this is the true core of the long Leontief Cycles.

With mainstream bourgeois economics the savings deposited by households as well as the anticipated economic growth through credit investment, and more specifically speculative credit with all its derivatives instruments, are confused within the so-called « universal bank ». This undermines the fractional system making it less reliable. However, as soon as the Central Bank agrees to bailout vulnerable speculative players, the cybernetic control mechanism played by the prudential ratio disappears and is substituted by the Central Bank’s recurrent intervention. During the early years of the neoliberal monetarist Reaganian counter-reform, Orange County went down and soon the Federal government and the Fed were forced to mop up the mess caused by the Saving and Loans Banks at a cost – unheard of at the time – of close to half a trillion dollars. But this looks benign in retrospect! Compare it to the recurrent bailouts by the FED or the ECB, this last moving from the original so-called transient – 12 months ! – Facility 1 and 2, to the EFSF, the ESM, the OMT, the LTRO, the TLTRO 1, 2, 3, to the APP, the PEPP, the EU IMF-like MES and to the New Anti-fragmentation instrument or Protection Transmission Instrument etc.. It is doubtful that this PTI will ever transfer more credit to the real economy than previous tools: as we know Draghi’s LTRO were offered, at least officially, with this stated aim; indeed, the funds had eventually to be reimbursed if that failed; when the deadline came, the highly vulnerable banks could not reimbursed and Mr « whatever it takes » came up with TLTRO 1, 2, 3 … Note that the LTRO allowed foreign banks, notably German and French, to lower their exposure to the Italian public debt, thus causing the dramatic explosion of Target II on top of the increasing public debt. Many Italian economists and commentators firmly believe that Target II is a mere « jeu d’écriture » !!!

It remains a moot point if such PTI funds would at least allow the banks to buy government’s bonds to keep the spread low. Lately, for countries like Italy, it is the ECB that does most of the buying. It does not stop here: To these oceans of liquidity we must add all the numerous national interventions used to recapitalise non-systemic banks, from the German Hypo Bank to the Italian Monte dei Paschi di Siena etc.

Incidentally, the recurrent bailout of MPS, of which the Italian State now owes 64,23 %, did cost so far more that 25 billion Euros in the last 14 years and past experience does not bode well for this pouring of public money in such a Danaids Sieve. In fact, the new 2,5 billion Euros market recapitalisation goes hand-in-hand with 4 000 layoffs ! The 35-hour labor reform of the « gauche plurielle », which directly and indirectly induced the creation of 2 million jobs paying social dues and taxes, did only cost 23 billion Euros a year… (See « Monte dei Paschi, la plus vieille banque du monde, boucle une augmentation de capital cruciale pour son avenir », La plus vieille banque du monde est parvenue à lever les 2,5 milliards d’euros nécessaires pour renforcer son bilan et financer son plan de réduction des coûts avec 4.000 départs attendus. La banque ne s’est jamais vraiment remise de la crise financière de 2008 et enchaîne les augmentations de capital pour un total 25 milliards d’euros levés en quatorze ans. , in latribune.fr , 04 Nov 2022, https://www.latribune.fr/entreprises-finance/banques-finance/banque/monte-dei-paschi-la-plus-vieille-banque-du-monde-boucle-une-augmentation-de-capital-cruciale-pour-son-avenir-939477.html .) One should equally consider the exemplary nationalisation of Northern Rock in the UK at the very beginning of the subprime crisis; only a very modest recapitalisation was needed given the role of the prudential ratio. The same happened initially in Iceland for the whole banking system.

Contrary to what is constantly preached concrete alternatives do exist. Indeed, both instances of national recapitalisation had no dramatic impact upon the growth of the public debt, a nice departure from the course of action followed by the speculative bailouts continuously carried out by our own speculative Central Banks. Note also that the mountain of derivatives in the shadow banking and other Black Pools does not appear into the banks books or into the formal financial system. Neither the Central Banks nor the BIS have an exact idea of how many there are out there. Some writers have hazarded that all the derivatives put together are approaching the quadrillion. OTC – around 600 trillion USD – are also known as scraps and are traded from hands to hands, just like it happens in horses races aside from the regulated betting platforms. Here competition still rules and losses purge the system without counting on the recurrent systemic bailout by the Central Bank operating in the « credit without collateral » regime.

When the prudential ratio works within the fractional setting, bank loans and economic growth – the more so when the speculative economy is not yet hegemonic – will be closely linked to credit expansion. Conversely, when growth slows down, credit necessarily shrinks. At this point, a regulated if only Keynesian economy would trigger counter-cyclical State investment in public enterprises and public infrastructures to restart the machine. However, the hegemony of speculative capital goes hand-in-hand with a Reaganian Minimal State – deregulation and privatisation – and its public policy mainly materialise in the form of lavish tax expenditures and of the regressive flat tax philosophy.

We saw above how the hegemonic speculative economy invades all spheres of economic activities to which it imposes its rules. At the same time a process of relative autonomisation is taking place as is reflected by the increasing size of the FIRE sectors in the GDP. The connection with the real economy becomes increasingly tenuous, both in terms of the respective weights and in terms of the accumulated reciprocal vulnerability. A simple glance at the public and private debt sustainability will illustrate the point. The Central Banks are now obliged to act to avoid the bankruptcy of both vulnerable States and vulnerable systemic financial players. The increasing relative autonomy of finance can thus be understood as a strategy to deny and delay the effects of a lethal contradiction. Hence, to display quarterly profits new rotations as invented, for instance, bitcoin, and excess money that cannot go into productive endeavors goes into the vicious circle of buybacks. At this point, this supposedly inextricable Gordian Knot of mutual vulnerability – speculation/enterprises/State – which causes so much headaches to academic, economic and political leaders alike, does in fact present the way out of the quagmire. Indeed, were a State willing to leave the management of money – with a proper definition of structural inflation – to the Central Bank and take back into its hands at least a part of the public credit allocation, it would soon isolate the most strategic part of the economy from speculation.

This can simply be done with the creation of a public bank with an initial prudential ratio of 40 to 1. Any State is able to budget 2 billion a year to be destined as the public bank own assets. This would allow the public bank to immediately use close to 80 billion in the form of credit to buyback and cancel the most onerous government debts circulating on the secondary market as well as to finance the needed re-capitalisation of nationalised strategic enterprises and of small businesses and cooperatives. As this would be done year after year for a sufficient duration, for instance 5 years, the economic and budgetary impact of the public bank will grow while the initial prudential ratio can be progressively lowered. Such a State would also tightly regulate the degree to which commercial banks can invest in the real economy, thus leaving former creditors to invest the funds they received in exchange for their government bonds into speculative endeavors, mainly in the biggest financial centres such as Wall Street and the City where they could play their Monopoly games between themselves. At this point, were a systemic bank to fail, no public bailout would occur but only the appropriate auditing. Bankruptcy would ensue to purge the speculative system – the only possible reset compatible with capitalist competition – thus allowing the public bank to step in to take possession of the failed institution at the symbolic cost of one Euro; this will then lead to a public recapitalisation aimed at saving small businesses and small savings. Unless, of course, the Central Bank and other big private players come up with a different scenario. In short, the autonomisation of speculation has gone so far that it is now possible to formally disconnect the real economy from the speculative leeches thanks to the rehabilitation of public credit.

Speculation is induced by the capitalist organization of credit and by its blind method to allocate socially scarce resources. Not only is credit confused for money but it is privately controlled. This ensures that the same acquisitive capitalist mind will move all the legally favored economic agents, be they entrepreneurs or bankers. If that were not enough, private property constitutes the core of bourgeois democracy. This ensures that all agents can pretend to the same formal conditions regulating access to credit both from the Central Bank and from private banks. It follows that the wealthiest players will de facto enjoy a better access to credit, proportionate to their wealth. The acquisitive mind of the bankers and financiers does the rest through the meta-magic and blind working of the « invisible hand ». Even in presence of a strict fractional banking system, more money will go into more dynamic – read « speculative » – sectors to the detriment of others until the time when the mobility of capital will reassert an intersectoral average rate of profit. John Galbraith has traced the history of these speculative crisis. (See A short history of financial euphoria ) This explains the extraordinary wastes of resources which is the way of life of the Capitalist Mode of Production in inegalitarian societies in which basic social needs are not universally satisfied.

This speculative working of ordinary capitalism was made worse with the legalisation of speculation that accompanied the abrogation of the Glass Steagall Act in 1999. Not surprisingly this quickly led to the subprime crisis of 2007-2008. The paradoxical conclusion of this unprecedented crisis, at least since the Great Depression, is fully contained in Treasury Secretary Paulson offering in March 2008 as a remedy to the crisis his report of March 2007, which contained all the elements that had led to that particular crisis. Unsurprisingly, it only took a few years to see the absurd ratios CDS/assets and OTC/assets becoming even more grotesque than they had been before the crisis. P/E ratios present the same disastrous picture. The casino economy had now transformed into a Monopoly Economy mainly rotating upon itself on the Stock Exchanges and in the opaque venues of shadow finance and other Black Pools. This vicious circle can be seen, for instance, with the billons of monthly buybacks on the official circuits. The result is the weakening off the other two summits of this Deadly Triangle, namely the fiscal revenues of the State and the real economy, which is now made worse in its current Quadrangle shape, a Quadrangle that adds exploding boursiarisation to speculative finance.

Central Bankers took note. There were talks of a « reset » or normalisation of the Central Bank’s balance sheets. Summers-Blanchard and al., had convinced the Central Bankers of developed countries to tend to a Zero Lower Bound for the guiding interest rates. They did so in the hope of mopping up the accumulated public debt on the back of foreign – mainly Japanese and Chinese – and of domestic creditors and savers while productive investment was replaced by buybacks and by the Financial-Insurance-Real Estate (FIRE ) share of GDP which increased obscenely. Quantitative Tightening was intended to follow the earlier lavish Quantitative Easing in all its shapes and forms. Meanwhile as we explained above the speculative economy was legally cannibalising the real economy while recurrent QE were inducing an ever greater Credit Crunch.

We know how this did end up. Even Tapering, let alone Tightening, proved difficult. First, Trump’s regressive fiscal policy did undercut Chair Powell’s initial attempt at reset by feeding more speculation – and capital evasion to fiscal paradises such as Bahamas etc. Soon, the sindemia due to SARS-CoV-2 and the ensuing explosion of UI requests forced the Trump Administration and its successor to come to the rescue thus palliating a dismantled American Social Security System. It seems clear that president Trump lost his election because, during the electoral campaign, he kowtowed to the more conservative wings of the GOP and lowered UI payments.

We have already documented elsewhere how these stimulus plans adopted in the context of the reaffirmed « credit without collateral » system led to the emergence of new roles assumed by repos and reverse repos as liquidity moderators with the proactive help of the FED which meanwhile was still talking of transiting out of QE through tapering. Repos reached 75 billion USD on September 2019 and continued to grow tremendously since then. The rise of reverse repos became even more dramatic after March 2020.

In the first instance there were justified talks of « transitory inflation » since a share of the federal stimulus accruing to the unemployed was used to buys used cars and to repay debts while an eviction moratorium was in place. I had earlier predicted a secular inflationary trend linked to the inept suicidal IPCC strictures and to the Paris Accord new obscurantist Credo. (See: http://rivincitasociale.altervista.org/paris-agreement-climate-decarbonization-and-the-problems-with-ets-the-climate-crime-against-emerging-countries-and-against-the-vast-majority-of-humanity-to-be-frozen-at-the-unequal-development-lev/ ) But the inflationary spike was clearly linked to the stimulus impact on disposable income, hence, mutatis mutandis, it was a transitory one. With these massive UI payments, the median US disposable income went up (!) and the poverty level reached the lowest point ever registered since Volcker-Reagan counter-reform of 1979-1982. But no academic cared to take notice. Because of the threshold established for these UI recipients, JP. Morgan had quickly calculated that more than 300 billion would end up to the relatively wealthy middle classes who would then be looking for the kind of financial investments more familiar to their kind of households. It adjusted in consequence, with the expected rippling effects. As for the first big reverse repos instance in March 2020 it seemed to have been provoked by the sudden drop of the bitcoin.

This transient inflation spike solidified thanks to other international events and Imperial lunacy such as the cruel sacrifice of Ukraine’s young population manipulated to fight lost exclusivist battles aimed at destroying all the economic and military rivals of the putative Empire, including Germany and the EU.

The willingness to accelerate the « ecological transition » with the implementation of the death of fossil energy sources and off associated industrial endeavors will make things much worse and quickly lead to the irreversible demise of the US and of Western Europe, now sacrificed as the new frontier of speculative capital accumulation just as Eastern Europe had been with the Treuhand and others. To fully apprehend this suicidal exclusivist process, one only needs to think it through in terms of economic coherence and in terms of employment lost in the sacrificed industrial sectors. « The way we were » seems like a forgotten dream …

The general situation is now worsening rapidly with the unfolding but poorly understood inflations – in the plural – and with the induced negative real rates of interest. In brief, one can consider the most significant relationships between each summit of the Deadly Quadrangle – speculative finance/stock exchange/State/real economy – for bonds and equities and then look at their general economy or sustainability, hence at their many contradictions and the ensuing bourgeois-academic mediations that only serve to compound the problems and delay their tragic outcomes. However, the ties characterising capitalist entrepreneurial and governmental behavior are now so obviously disconnected that the current elite is navigating blind and feeding into the acceleration of the socio-economic crisis complete with its economic theoretical rout.

Increased interest rates affect the value of bonds on the secondary market in inverse proportion. Increased negative rates make things worse forcing margin calls to rebalance the books; the Central Bank, unwilling to raise rates at the level indicated by the textbooks – that is, more than the CIP and, in fact, much more given the reactive lag – is forced to intervene since the mountains of bonds used as collateral on the market would cause a series of systemic events among financial players. All of them are thus left hanging in midair and using rotations on the Stock Exchange to show some results on their quarterly reports, making this part of the Monopoly economy even more bubbly. Layoffs are massively used to lower the salary mass seen as a cost. Meanwhile, to quiet the markets which had been fed textbook junk-food on inflation – in the singular – up until now, alongside a plethora of other such Marginalist vacuous concepts, the Central Bank is « forced » to go along. (Remember Acheson, who had been « at creation », calling Maccartysts « animals » just because they failed to quickly adjust to the new Detente climate, forgetting that he, Dulles and others, had fed them in the first place ?)

The Central Bank is now banking on communication to keep a semblance of the control which in fact it has utterly lost. The « psychology » of the markets is turning away from perception toward reality and becoming more ground-to-earth! To cause as little damage as possible the focus is squarely placed on core inflation only, which is ingenuous at best. In so doing it sends the economy into a downward spiraling path, albeit at a slower pace. Naturally, this causes recession while at the same time drastically reducing investment in the real economy, with the expected series of consequences on the balance sheets of banks and funds – deindustrialisation, zombies companies etc – and on the fiscal revenue of the State. In the end, the taxpayers are the sole lender of last resort.

To counter this trend, the Acceleration of the Ecological Transition is now played to the maximum . This is an added fallacy. See the opaque financing of the Stop Oil campaign and similar groups of nihilist militants by various foundations, https://www.theguardian.com/environment/2022/apr/29/just-stop-oils-protests-funded-by-us-philanthropists ). We have already explained that this green speculation and the irrational regressive regulation wished for in the framework of the Paris Accord fly in the face of the expected results. For one thing, this transition is more polluting than the old fossil industries – even in terms of CO2 – and leads to price and technical absurdities; one only needs to think of the electrical car here in order to understand the magnitude of the damage caused by this narrative mess. (See prof. Gerondeau : https://www.youtube.com/watch?v=zd9ps7ISHl8 . Add that there are no used electrical cars since every 7 years more or less one needs to change the increasingly expensive battery, all these cars requiring an exponential amount of electricity …)

Add to it the irrational warmongering sanctions imposed on Russia … in order to destroy Europe as a major economic rival of the putative exclusivist Empire as well as Russia and emerging countries around the Globe. As the recession accelerates toward a full-fledged Depression, unemployment increases, both in the official and obscene ILO sense and in real terms, as demonstrated for instance by the lower rate of occupation and the dramatic increase of absolute and relative poverty. In turn this causes a drastic diminution of the social dues which finance the counter-cyclical and organically anti-inflationary programs of public Social Security and it drastically decreases of fiscal revenues of the State. In short, this rigmarole ends up feeding into all the other contradictions. This is because the huge extend of necessary stimulus used to marginally protect households ends up feeding all inflationary – and anti-environmental – processes. This is due to the refusal to return to a strict and general Cola clause, and to the insistence on wasting huge amounts of money that are now used to finance the speculative Green New Deal strategy.

We get the general sense of the current Marginalist speculative folly. As the remaining public regimes of Social Security are attacked and privatised, in particular the lucrative public pension and UI schemes, one needs to point to the obvious: The current crisis in the UK with the forced resignation of the Chancellor of the Exchequer and soon after of PM Liz Truss was squarely centered on the British privatised pension funds and their speculative investments. This could never have happened with the public pension scheme similar to the ones still present in France or in Italy which are run according to a strict repartition philosophy, hence with the afferent public and mutualised actuarial rules. Despite this evidence, which should send some back to the bankruptcy of such private schemes that happened during the Great Depression or to the transformation of 401K into 201K in the USA with the unfolding of the subprime crises, the same main players, which caused the British recent crisis, such as BlackRock, are still pressuring governments in the EU to privatise their remaining albeit already shrinking public and safe pension regimes!!! Go figure …

Let us now briefly examine the UK, the EU, the Spanish and the US current strategies

The speculative attack against the UK in September, 2022. It surpassed in gravity the speculative attack on the pound that unfolded on September 19, 1949 when the US Administration forced the Keynesian British authorities to bury their veleities to reengineer the old Imperial Preferences in the guise of the post-1936 and post-war reorganised Commonwealth in order to impose the Washington-dominated Gatt world regime. In the current instance no political accommodation can solve the underlying contradictions. Each player follows its over-determined speculative logic.

Ms Liz Truss did everything she could to please the markets, from the added tax expenditures, offered in the framework of a sanguine flat tax philosophy, to the stimulus plans devised to assuage the weight of the crisis and of the inflationary crunch on the households, if only because of the announced strikes and of the rise of the Labor Party in the polls. Accurate budgetary arithmetic is no longer in the card given the systemic multi-faceted uncertainly that makes economic previsions hazardous at best. From governments to capitalist Central Banks every one now recognises that econometric models are useless – see Romer’s critique in his January 5, 2016, 25 pages essay … Indeed, in the EU, the Fiscal Compact and even the 3 % deficit ratio of the Maastricht Treaty have been quietly thrown in the garbage pail, and no one, especially not the current EU Commission, will say boo as long as the previous class-oriented austerity policies are maintained. In Italy, the Articles 81 and 97 of the Constitution, which imposed strictly balanced budgets at the national and at the local levels, are quietly flying out of the window but, of course, this does not mean that real counter-cyclical public policies will be implemented; it only means that more rope is given to the current neoliberal monetarist leaders to continue imposing their austerity programs to the masses. Even « forward guidance » has generally been abandoned in favor of « meeting to meting guidance » by the FED and the ECB.

In the UK, the problem was basically triggered by Blackrock and other speculative agents heavily invested into the British pension funds; their sole consideration was their balance sheets given the negative real interest setting. This was enough the trigger their marginal calls causing other players to follow suit. I believe that the « defensive » move was equally intended to force the BoE to end its QT and buy all the Gilts unleashed on the market.

Like the rest of them, the BoE is now engaging in a disconnected irrationally pseudo-practical policy of slowly raising interest rates in an failed attempt to influence the Core inflation, and its obligation to redo QE in many forms in order to avoid many systemic events. Of course, this includes global agents like Blackrock in the aggravated context of reverse carry trade induced by the rising USD. Which explains the recent line of credit swap from the FED to the BoE. We will soon see what the new British PM., a Goldman and Sachs’ Boy, like Draghi, will do. Think of Paulson delivering in March 2008 his speculation-favoring March 2007 report as a remedy to the subprime crisis which it helped to feed! Poor GB is not great anymore. As Keynes said when landing in Kennedy airport during WW II: « Boys, Britain is broke » (to which FDR responded « You can still sell Newfoundland! »). Not great anymore unless, of course, a revitalised Labor and Corbyn are coming back … (On the UK crisis, see:

a ) « ‘I’d never seen anything like it’: how market turmoil sparked a pension fund selloff », Bank of England stepped in on Thursday to stabilise price of UK government bonds and avert a deeper crisis, Sept 29, 2022 https://www.theguardian.com/business/2022/sep/29/id-never-seen-anything-like-it-how-market-turmoil-sparked-a-pension-fund-selloff

b ) « “Forced Selling Of Everything” – UK Pension Funds Are Still Liquidating Assets, Seeking Bailouts », by Tyler Durden, Friday, Sep 30, 2022, https://www.zerohedge.com/markets/forced-selling-everything-uk-pension-funds-are-liquidating-assets-seeking-bailouts

Signs of the time: On November 3, 2022, the BoE came up with a moderate hike of 75bp of its key interest rate while attempting to quiet the markets stating that « further increases will be necessary to meet our goal, however the peak will be lower than the market expects,” she said in a summary of her meeting.» (« L’annonce de la hausse des taux de la Banque d’Angleterre fait plonger la livre »

La Banque d’Angleterre a annoncé ce jeudi relever ses taux directeurs de 75 points de base à 3%. Une annonce qui a fait chuter la devise britannique. Elle frôlait les 2% de perte face au dollar et plus de 1% face à l’euro. L’institution avait toutefois pris soin de tempérer les attentes du marché, signalant que celui-ci surestimait sa volonté de poursuivre des hausses qui pèsent sur l’économie.

latribune.fr, 03 Nov 2022, https://www.latribune.fr/economie/international/l-annonce-de-la-hausse-des-taux-de-la-banque-d-angleterre-fait-plonger-la-livre-939383.html

The BoE is no longer followed by the markets which are trying to impose their private-oriented will on it. The BoE tried in vain to massage the market psychology by declaring that «further increases will be necessary to meet our target, however the peak will be lower than the market expects,” she said in a summary of her meeting.». It had the opposite effect… The markets disagreed and pushed the pound down. Remains to be seen what the new PM will do …

Let us now look briefly at the EU. The quagmire facing M. Jerome Powell’s and the other central bankers’ attempt at reset was already analysed in my « The FED DILEMMA, or how the Marginalists are now trapped into their own shameful narrative », Sept/Oct, 2015, International Political Economy, www.la-commune-paraclet.com. In a text written last May and reproduced here partially in the Annex, I analysed how the FED was in such a predicament that it could not even carry out a total tapering. Then, given the general ineptitude that would still pretend, despite plain facts, that « inflation – in the singular ! – is always and everywhere a monetary phenomenon », I felt the need to summarise the three main kinds of inflation that had been analysed in detail in my Synopsis of Marxist Political Economy and in my Methodological introduction both freely accessible in the Section Livres-Books of my old experimental site www.la-commune-paraclet.com. The motto of this site is that Marxism is science and vice versa, especially for social sciences – or else I would not have lost my time with it. Now if you go against science, you go right into the Wall. That summary can be found here: « Quick comment on inflation, QE and public debt, rotations, repos and reverse repos », May,27, 2021/ in http://rivincitasociale.altervista.org/a-quick-comment-on-inflation-qe-and-public-debt-rotations-repos-and-reverse-repos-may-27-2021/ . Today’s event can be seen as the Epilogue that confirms my analysis. Finally a word will have to be said about the mounting debt crisis in the emerging countries, tragically hit by the USD carry trades just like it had happened under Volcker-Reagan, except that today’s they can count on China and the Brics +.

At the light of the events unfolding in the UK, the ECB quickly sized the problem caused by negative real interest rates for hegemonic speculative finance; but meanwhile it has to stick to its albeit fallacious, policy of calibrating rates hikes to the Core inflation, a delaying strategy at best, but one ideated to avoid a sudden and catastrophic recession. (See in particular: « ECB « Monetary policy decisions », October 27, 2022, https://www.ecb.europa.eu/press/pr/date/2022/html/ecb.mp221027~df1d778b84.en.html )

There are now talks of a supposed « neutral rate » of interest best able to conciliate its level with the sustainment of economic activity compatible with a progressive lowering of the Core inflation to 2 %. Such talk of « neutral rates » brings to mind Wicksell’s efforts to conciliate A. Smith and A. Marshall, something not quite in tune with current speculative Marginalism; in the end, it looks like squaring the circle, no one really knows how to do it but they still try to approach the problem geometrically and empirically. To me it looks like Mandelbrot, the ineffable pitre who searched for God’s Equation in his fuzzy logic, meanwhile trying to apply stochastic analysis to the Dow Jones data taken as hard economic data!

The road to the reversal of QT is now opened since the bonds arriving at maturity will be reinvested and we know that, despite its status and the ECB internal quotas, it holds more bonds from the most vulnerable countries like Italy. Meanwhile APP and TLTRO will be indexed and we know that new emissions are also largely indexed, contrary to wages etc. On top of it all, reserves deposited at the ECB in compliance with the formal fractional banking system, will continue to be remunerated. This is an obscene gift to the private banks which doubles into an absurd twist to the normal working of the logic of the prudential ratio. In fact, such remuneration began after WW II with the internationalisation of productive capital, mainly US Multinational corporations – MNCs –, a trend followed by US banks’ expansion abroad. To reinforce the USD in the framework of the Bretton Woods System – convertibility of the dollar for gold, namely 35 USD for one Ounce Troy of Gold – and of the US-dominated GATT, Washington offered foreign Central banks a remuneration on their reserves held in USD. Such a system makes no sense within the EU and amounts to yet another gift to speculative capital, a very onerous one at that as long as inflation in the CPI sense will remain way above the Maastricht Treaty 3 % limit.

On the governments’ policy side, as the full Cola clause is foolishly pushed aside, it will all hinge on how the necessary governmental aids to households and economic stimulus plans will be financed. New debt will directly feed inflations especially that part that goes to households which will ultimately pay the cost twice, first as consumers and secondly as taxpayers; conversely, when the aids and stimulus plans are paid for organically through a more equitable sharing of the « social surplus value » – and not only partial sectoral windfall profits – the inflationary impact is cancelled at the source.

As a matter of fact, that piece of real economic science, which was derived from the lessons learned from the Great Depression, had been enshrined in our post-WWII Constitutions in the form of progressive taxation and State intervention in the economy when the private sector proved unable to deliver the constitutionalised Social services that had now been proclaimed as Fundamental Social Rights. The neoconservative fiscal policy and its flat tax philosophy and billionaire tax expenditures for the private enterprises and the wealthiest are really in violation of the letter and spirit of our advanced democratic Constitutions.

As credit is an anticipation of economic growth, it might be argued that it contributes to the creation of real exchange value, hence it would play a anti-inflationary role. This was true for public credit emitted almost free of charge by the public central bank. Because it was publicly owned, it did not have to pay shareholders or other markets leeches. In the real economy, public credit transforms on average for 60 % into an increased real salary mass – plus social contributions and taxes – thus sustaining internal demand and for the rest into immobilised, fixed real capital in the form of public infrastructures which in turn contribute to the macro-economic competitiveness of the Social Formation hence to the micro-economic productivity of the private sectors. The post-WW II rapid Reconstruction of France and Italy which was made possible with very low resulting public debt and significant real growth proves the point without the shadow of a doubt.

(This important graph was already quoted in : http://rivincitasociale.altervista.org/rapport-arthuis-2021-vous-avez-aime-thatcher-reagan-vous-aimerez-arthuis-version-italo-ludwig-mises-5-mars-2021/ )

It is no longer the case since credit is speculative and as such it cannibalises the real economy. Even the public debt emitted by taking advantage of the better international EU rating to finance the Recovery Plan with the PNRR funds will prove disappointing if only because 30 % will go into the destructive climate transition and another 20 % into the digital economy which relies largely on imported components.

To add insult to injury, the Fiscal Compact is suspended de facto sine die given that low growth makes it impossible to reduce the portion of the public debt over 60 % of GDP by 1/20 a year. Simultaneously the current budgets now presented by the member States to the EU Commission for approval are built mostly around or above a 5 % budget deficit, that is to say much higher than the 3 % Maastricht Treaty limit. (In Italy, no one dares ask the definitive burial of the inapplicable Reaganian Articles 81 and 97 of the Constitution modified in 2012 to fit the neoliberal monetarist philosophy of the Maastricht treaty.) One would normally applaud thinking that, in such a case, the opportunity is finally granted to member States to come up with a real and rational budget capable of restabilising economic good sense and growth while respecting constitutionally enshrined social rights. But this is not the case. No academic, no economist, no political representative dares to even note the de facto joint burring of the Fiscal Compact’s and of the budget’s limits. All continue backing the worst neoliberal monetarist austerity measures with more linear cuts into social and public spending and more ruinous tax expenditures, on top of which, in subservience to Nato’s warmongering, are now stacked more military spending despite the very low economic Multiplier of such spending, especially when it is not directed into dual military-civilian use.

As already underlined in my « The FED DILEMMA, or how the Marginalists are now trapped into their own shameful narrative », Sept/Oct, 2015, International Political Economy, www.la-commune-paraclet.com , we are now witnessing the brutal demise of the absurd neoliberal monetarist pretense according to which monetarist polices can manage the whole socio-economic sphere by themselves. Hence these policies are pursued by autonomous Central Banks firmly placed in the hands of the speculative hegemonic finance, in the hope that they can substitute for both monetary policies – hence at a minimum the scrupulous implementation of the cybernetic logic of the fractional ratio – and for budget and economic policies – with progressive taxation instead of tax expenditures for the rich and with State interventions when the private sector cannot deliver.

The remaining question to ask is: given the aforementioned Deadly Quadrangle what are the main weak points? The current speculative attacks on the British pound should have alerted the EU member States which are still ideologically sold to the further privatisation of remaining social security programs, in particular pensions plans. This is something Blackrock and other such speculative funds have been demanding for years with the undemocratic active complicity of the EU Commission which is here acting out of its precincts since Social Affairs fall squarely into the exclusive national competence of member States. Additionally as recession is slowly but surely imposed by the Central Bank with its fallacious insistence on Core inflation, increased unemployment implies the implosion of social services financed out of social dues as well as the destruction of fiscal revenues. Meanwhile, despite many zombie companies kept on the books of weakened banks to avoid onerous write-offs and possible bankruptcy, increased bankruptcies will add billions of outstanding State warranties to the public debt. The spread will rise as well as the increased weight of the public debt financing, and so on and so forth. Nothing here is sustainable … not even with billions of destructive New Green Bonds.

It would have been highly useful to look at Spain’s performance but at this point we do not have the necessary information to do it properly. What we know however is that Spain is doing better on many scores, both on the inflations front and on the economic growth front. Although the economy is slowing as everywhere else in the EU and the OECD, still « Compared to the same quarter last year, the Spanish economy grew 3.8%, the least in over a year. » (https://tradingeconomics.com/spain/gdp-growth ). CPI inflation did fall somewhat : « Spain’s consumer price inflation fell to 7.3 percent year-on-year in October of 2022 from 8.9 percent in the prior month, well below market expectations of 8 percent, a preliminary estimate showed. », (https://tradingeconomics.com/spain/inflation-cpi ).

But what is more important is Spain’s ingenious labor policy which transformed part-time work into full-time work. As of July, 2022, Spain had created more than 780 000 full-time jobs with the attached socials dues, taxes and increased internal demand. (See : https://www.francetvinfo.fr/monde/espagne/emploi-jamais-l-espagne-n-avait-cree-autant-de-contrats-a-duree-indeterminee_5263462.html )This allowed it to raise pension levels by 2.5 % and by 3 % for the lowest pension brackets this year and even to grant public transport free of charge to the end of this year. The least that can be said is that Spain made a judicial use of the 12 billion Euros from the European fund destined to lower work precariousness.

As we know, aside from being less depended on Russian gas or more accurately less affected by the suicidal sanctions the EU imposes on Russia, Spain wisely suspended its participation in the ludicrous EU’s unique energy market. It was then able to slash energy bills by 30-40%. Unfortunately, the suspension is due to last 12 months only. (see https://www.express.co.uk/news/science/1617152/energy-crisis-spain-portugal-break-ranks-russia-climate-change-uk-bills )

It would seem that the Spanish government has understood the sheer foolishness of the EU unique energy market; it is based on the absurd « last producing unit called » into production for a given energy market deal, something totally different from the already fallacious Marginalist « marginal utility ». In fact, here we are dealing with an administrative structure that fixes by design the price for all players at the highest level, the last producing unit called being usually based on gas or coal production; these are generally the most expansive especially today with the EU Carbon taxonomy and the suicidal sanctions imposed on Russia. The system is solely devised to financially sustain badly inefficient and intermittent renewable sources of energy. This is not Dr Sum’s administrated prices used as a way to forbid and control usurers; on the contrary, it is the typical reversal, here of Thomist intentions, devised to implement administered prices designed to operate in favor of the speculative usurer’s behavior … simultaneously aiming at the acceleration of the suicidal ecological transition supported by the IPCC a-human narrative which turns CO2 production into a new original sin just because life on Earth is carbon based!

The same was done in the Jewish Old Testament with sex just because the Human Species is a Species based on sexual reproduction. If you turn something natural and unavoidable into a SIN then all are guilty by definition and all need to atone by following the Great Priests’ and their Lower Clergy’s enforced intermediation, in this case enforcing mass frugality with the brutal lowering of their « rising expectations ». As usual, the wealthiest can amend by buying the proper indulgences. As we know, many wealthy foundations – including Aileen Getty’s – are now heavily financing the Just Stop Oil campaign and the nihilist militants’ road map to accelerate the transition. (See https://www.theguardian.com/environment/2022/apr/29/just-stop-oils-protests-funded-by-us-philanthropists . One might also want to see this link and the incorporated short videos – remembering however that the use of the word « left » seems quite inappropriate, at least to me; corporatist fascism seems to me to be more acurate – Greta Thunberg Calls For “Overthrow Of Whole Capitalist System”. by Tyler Durden, Tuesday, Nov 01, 2022 – 03:20 PM, Authored by Paul Joseph Watson via Summit News, https://www.zerohedge.com/geopolitical/greta-thunberg-calls-overthrow-whole-capitalist-system )

Together with the IPCC fallacies embodied in the Paris Accord, these self-appointed World leaders are the direct cause of the initial and continuing rising of energy prices which feed the inflationary processes. They further propose to quickly kill the fossil industries; the only problem they see in so doing is to save the banks’ fossil assets. They thus propose to create a bad bank and to substitute the fossil bonds with new Green Bonds, naturally paid for by the lender of last resort namely the taxpayers. Not a word is heard about the fate of all the people working directly and indirectly in these sectors and in the other connected industries. Not a word is heard on the bigger pollution – including in terms of CO2, water and other pollutions – induced by the intermittent sources of energy or about the sheer disaster accompanying the transition to the electric car. Can you just phantom a modular nuclear plant every 100 km on the Highways, for a type of car that will cost much more than an efficient combustion engine car and for which there will be no used car market since the increasingly expansive battery needs to be changed every 7-8 years? Add to this, the restriction on mobility enforced by limited circulation zones … « Laissez faire, laissez circuler »? Not anymore, we have entered into regressive post-capitalism, « once again » …

Seen from this angle it seems that « inflation » is equally used to mesmerize citizens to force them into the new « road to serfdom » that of the society of new slavery and new domesticity already announced by the late Sixties Establishment’s Report from the Iron Mountain and retaken in so many shapes afterwards, for instance by the Trilateral Commission complete with its call for the « end of rising expectations » of the citizens and workers or its invention of the bloody Strategic hamlets strategy, its « clashes of civilisations » and the on-going implementation of the illegal and criminal Doctrine of preventive war aimed at destroying 66 Muslim States as well as all the economic and military rivals of the putative exclusivist Israelo-American Empire, the EU and Germany being now included in the list with the instrumentalisation of the war in Ukraine.

Let us now look briefly at the USA. It will suffice to provide few crucial statistics to see the unfolding catastrophe and why many people from the Left to the Right, overtaken by a legitimate nostalgia about « the way we were », might deplore the interruption of FDR’s New Deal that was focused on Social Security programs firmly anchored in the growth of the real economy, an interruption which started with the electoral defeat of Wallace by Truman in 1945. These statistics must be read in their evolving dynamic. It is that of the « credit without collateral » at the epoch of negative real interest rates.

In what follows numbers are taken from https://tradingeconomics.com/ unless otherwise indicated.

The « Government Debt in the United States increased to 31 238 301 USD Million in October from 30 928 912 USD Million in September of 2022. » .

The Debt/GDP ratio equals 137.20 % (2021)

The Federal budget deficit is at 16.70 %

Some people have provided useful projections for the increased weight of the public debt financing. It will be somewhere between USD 1.1 to 1.4 trillion a year, much more than the ludicrously high – the poorest Multiplier of all – military budget (754 billion for 2022.) See for instance :

« Payback’s A Witch

The sell-off in long-dated Treasuries isn’t because of last year’s inflation. It’s because the market knows that the U.S. Treasury cannot possibly afford a real rate of interest on its massive $31 trillion in debt.

Think about it: this year’s increase in Social Security benefits payments is 8.7%. At even half that rate of inflation, a 2% real yield on a 10-year U.S. Treasury bond would be well above 6%. If the U.S. government has to pay anything like that rate of interest to roll over its debts (average duration is 5 years) in the coming years, it is already bankrupt.

There are $24 trillion worth of publicly traded U.S. Treasury securities. At 6% interest, that’s $1.4 trillion a year in payments. That’s roughly 40% of total federal tax receipts. » (https://www.zerohedge.com/markets/how-bernanke-broke-world )

The interest rate is at 4.00 % while the inflation rate is at 8.2 % (Sept. 2022). Core inflation is at 6.6 % « the highest since August 1982 ». Real interest rates are negative.

To assess the real inflation rate felt by households, even more than by enterprises, it is useful to look at the numbers provided by http://www.shadowstats.com/alternate_data/inflation-charts . It is double the official number.

Federal spending has increased tremendously « Last week Joe Biden announced that $1 billion in federal grants would be generated for manufacturing, clean energy, farming, biotech and other industries in 21 regional partnerships across the US. The money is part of a $1.9 trillion covid relief package that was instituted way back in March of 2021. That’s right, if you thought the covid funds were gone for good, you were mistaken. While certain elements of the original covid stimulus packages have dried up, there are still vast sums of fiat dollars being held in the coffers of various federal and state programs. (…)

In 2020, over $6 trillion of stimulus money was created from thin air by the Federal Reserve and injected directly into the US economy by Donald Trump (and continued by Joe Biden) through covid relief checks, PPP loans and bailouts for numerous corporations. Again, in 2021, Biden instituted the ‘American Rescue Plan Act’ which added $1.9 trillion to the pile. That’s at least $8 trillion in helicopter money dropped on top of the US economy.» (« The US Economy Is Still Being Artificially Supported By Trillions In COVID Stimulus », by Tyler Durden, Tuesday, Sep 06, 2022 , https://www.zerohedge.com/economics/us-economy-still-being-artificially-supported-trillions-covid-stimulus )

Most of it is coming from deficit spending and will feed the inflationary processes unless it goes into the real economy. By real economy we basically mean production of tangible goods and of services offered by the public administrations, something which is wrongly seen as a cost in the fraudulent Marginalist GDP, see http://rivincitasociale.altervista.org/gdp-marginalist-narration-tool-against-the-welfare-of-peoples-and-the-prosperity-of-nation-states-may-24-2020/ .

Although we are not able at this time to assess the destination and impact of these public funds in enough details, we know from earlier experience with President Obama’s stimulus plan that the Economic Multiplier was around 3 when the funds went into public endeavors – social services, education, bridges, roads etc – and only around 1, à la R. Barro one might say!, when they went into the private sectors, including private health and private schools. (see THE BODY ECONOMIC: why austerity kills, by David Stuckler and Sanjay Basu, HarperCollins Publishers LTD, 2013. A critical review. in https://la-commune-paraclet.com/Book%20ReviewsFrame1Source1.htm)

We also know that close to 500 billion will go directly into the suicidal green transition which will soon present us with a curious case study: it will prove how credit as the anticipation of real economic growth will, in this case, destroy the macro-economic parameters hence the micro-economic performance or productivity of the individual enterprises. We already made the point in our critique of the Paris Agreement, see : http://rivincitasociale.altervista.org/paris-agreement-climate-decarbonization-and-the-problems-with-ets-the-climate-crime-against-emerging-countries-and-against-the-vast-majority-of-humanity-to-be-frozen-at-the-unequal-development-lev/ .

One can already note how the USA autonomy in energy nevertheless transforms into high prices that consequently impact all production, transport, selling and consummation processes because it is abandoned on the speculative global market without any federal regulation except the occasional manipulation of the strategic reserves. It reminds me of the argument made by Robert Heilbroner in the mid-80 in an article published by the New York Review of Books in which he argued that there was no real fiscal crisis of the State, at least not in the USA; to realise it one only needed to compare taxes on gasoline in the USA and in the UE. Moreover we know that the « credit without collateral » speculative regime goes hand in hand with Reaganian neoliberal monetarist tax expenditures and with a ferocious workfare. Now even refineries are closing in the US. In brief, the US is now wasting his advantage both in term of energy autonomy and in term of imported inflation despite a stronger dollar.

Tax expenditures amounted to 1.5 trillion in 2016 (https://budget.house.gov/publications/report/what-you-need-know-about-tax-expenditures; the details for 2022 are provided here: https://home.treasury.gov/system/files/131/Tax-Expenditures-FY2022.pdf ) But this amount corresponds to what is still under the budgetary radars, worse yet it makes abstraction of capital evasion which probably amounts to around 3-4 trillion in the Bahamas alone. We know that « The USA loses nearly $190 billion to tax evasion every year. » and that « The world’s wealthiest keep $21-$32 trillion of personal assets in offshore tax havens. » (see https://balancingeverything.com/tax-evasion-statistics/ )

The greatest share of these tax expenditures goes to private enterprises and to the wealthiest. Although they are highly inefficient in terms of economic and social levers, tax expenditures are very well behaved – bon chic, bon genre, you know … – since once they are granted they tend to disappear from the fiscal revenue radar unless they can be used as legitimising social tools. Their contribution is mainly seen in the strongly inegalitarian redistribution of wealth rather than in its creation. They are the pulsating heart of the neoliberal monetarist public policy.

As we know the Volcker-Reagan counter-reform aimed at the destruction of collective bargaining and of the « rising expectations » of workers and citizens in favor of the re-establishment of the USD international dominance following the demise of the Bretton Woods regime, de facto on August 15, 1971 and de jure in 1976 at the Jamaica Summit. The double-digit interest rates and the torrential carry trades induced forced a realignment of all countries on Washington and explain the implosion of the Eastern Bloc countries that were more exposed to the international markets, in particular Poland, Romania and Yugoslavia. On the domestic front, they induced a strong and lasting recession and the US collective bargaining system – industrial democracy even in the minimal Dahrendorf, Dunlop and Kerr’s versions – was reduced to naught; unemployment seemed to subside with time but it was only a bad illusion because it meant that full-time jobs were replaced by part-time jobs which now take the obscene form of gig (or « shitty » ) jobs in the so-called Hegemon country.

Contrary to what is believed, inflation did not disappear because in reality it was masked by a reduction of social spending enforced by a brutal workfare. To ensure that there would be no government social spending slippage, the zero-deficit rule was imposed at the States’ level. We have here a typically skewed mediation: a contradiction – here inflation – seems to be solved but only at the cost of creating a bigger contradiction, namely here it causes fast growing precariousness and generalised wage deflation without the least sharing of the productivity gains. (See « The socio-economic consequences of MM Volcker-Reagan and Co » in http://rivincitasociale.altervista.org/another-america-possible-feb-1-2017/ at the light of the last paragraphs of former FED Chair Burns in 1979 https://www.scribd.com/document/519243182/The-Anguish-of-Central-Bankers-1979?utm_campaign=GoldFix&utm_medium=email&utm_source=Revue%20newsletter . One might then want to read this on inflation : http://rivincitasociale.altervista.org/a-quick-comment-on-inflation-qe-and-public-debt-rotations-repos-and-reverse-repos-may-27-2021/ . And this on the dismantling of the Welfare State : http://rivincitasociale.altervista.org/the-dismantling-of-the-social-state-or-of-the-anglo-saxon-welfare-state-and-monetarist-neoliberal-policies-seen-from-the-angle-of-the-labor-contract-october-4-2016-april-9-2020/ )

Today Western societies taken over by overpaid and over-represented exclusivist groups are betraying the very foundations of our civilisation. Instead of progressing, in one way or another – many roads lead to Rome as the saying goes –, towards emancipation and happiness as Thomas Paine’s Rights of Man and the Constitution would have it, we are forced into New Laws of Manu, complete with a transhumanist attack on the integrity of the Human genome. (See for instance « Nietzsche as an awakened nightmare » in https://la-commune-paraclet.com/livresFrame1Source1.htm#livresbookmark ; one the transhumanist Covid mass experiments, see the pertinent articles in http://rivincitasociale.altervista.org/category/another-america-is-possible/ )

There remains to say a word about unemployment. The official rate is given at 3.70 %. But this is the fallacious rate established according to the ILO parameters by which one hour worked during the last – subjective – evaluation qualifies you as an employed person. The real number of the unemployed and under-employed must take into consideration discouraged people, un-chosen part-time, the army of self-employed, the increasing black or illicit labor market, the millions of so-called « aliens » without whom the economy would grind into a sudden halt, as well as the cohorts of prisoners etc. For a more complete exposition see the Note ** in my Livre-Book III in the Livres-Books section of my old experimental site www.la-commune-paraclet.com .

Today things are so bad that official statistics become useless as they count jobs instead of workers! See, for instance, the clarification offered on the late numbers provided by the BLS just before the Midterms: It seems that instead of the employment gains announced, most newly created jobs turn out to be part-time while « Finally, the cherry on top: the number of Unemployed workers – also tracked by the Household Survey – jumped by 306K, rising to 6.059 million, the highest since February! » in « Something Has Snapped: Unexplained 2.3 Million Jobs Gap Emerges In Broken Payrolls Report », by Tyler Durden, Friday, Nov 04, 2022 – 11:18 AM, https://www.zerohedge.com/markets/something-has-snapped-unexplained-23-million-jobs-gap-emerges-broken-payrolls-report

In the current inflationary context we are witnessing an increase in paid hobbies by employed workers and employees, or multiple jobs holders, who are thus trying to fight the impact of real inflation on their standard of living given the absence of a generalised Cola clause. This in turn pumps up the official employment statistics. « Something very odd emerges for the second month in a row when looking at the July payrolls report. » (…)

« The increase for June? 92K, which stands in stark contrast to the sharp drop in full-time job holders. But even more notable is that since June, the US has lost 141K full-time jobs, 78K part-time jobs, while adding a whopping 263K multiple jobholders. » (See « Something Snaps In The Job Market: Multiple Jobholders Hit All Time High As Unexplained 1.8 Million Jobs Gap Emerges », by Tyler Durden, Friday, Aug 05, 2022 – 10:25 AM, https://www.zerohedge.com/markets/something-snaps-job-market-multiple-jobholders-hit-all-time-high-unexplained-18-million )

It gets worse when one looks at the participation rate at 62.2 % – October 2022 , https://tradingeconomics.com/united-states/labor-force-participation-rate – and at the poverty rate: « The national poverty rate was 12.8% in 2021, but was significantly different for the nation’s oldest and youngest populations, according to a new Census Bureau report released today.»

It might be useful to note that the participation rate – same link – hovered around 60 % in the 60s and the 70s when we had full-time full employment with only frictional and seasonal unemployment . (see: https://en.wikipedia.org/wiki/File:U1-U6_unemployment_rate.webp ) The apparent paradox vanishes when one looks at gender distribution : https://en.wikipedia.org/wiki/Labor_force_in_the_United_States#/media/File:US_Labor_Force_Participation_Rate_by_gender.png

In fact, up until the finishing 70s, one wage earner in a household was earning more than two in today situation, and they enjoyed more social protections, which meant that their individual net salary was going further because Social Security freed the households from the fear of the « rainy days » and from market swings transforming 401K into 201K. This also tells you a lot about the lack of labor parity and the half failure of the Marginalist restricted demand for « equal pay for equal work » without total parity. These restricted Marginalist demands are compatible with the neocon vision of « token » and even of « surrendered » women, a form of « pink quotas ». Add to this the underdevelopment of the socialisation of domestic chores through the furthering of Social Security public programs – for instance, national public kindergarten, old-age care and home care, etc. These are still mostly carried out by women and quietly amount to the equivalent to 1/3 to ¼ of GDP (Louise Vandelac, 1985)

As expected in the absence of a general Cola Clause, real salaries are going down. In July 2022 it was reported that : « US Consumer Prices Soared In June, Americans’ Real Wages Fall For 15th Straight Month », by Tyler Durden, Wednesday, Jul 13, 2022, https://www.zerohedge.com/personal-finance/us-consumer-prices-soared-june-americans-real-wages-fall-15th-straight-month

The child poverty rate (for people under age 18) was 16.9% in 2021, 4.2 percentage points higher than the national rate, while poverty for those aged 65 and over was 10.3%, 2.5 percentage points lower than the national rate. » in https://www.census.gov/library/stories/2022/10/poverty-rate-varies-by-age-groups.html

Inequality is reaching epic proportions. Pigou’s Wealth Effect simplistically offered as a critique of Keynes’s General Theory of employment, interest and money totally ignored the structure of revenues and its impact on harmonious economic growth. Luckily, Pigou was ignored as long as Keynesianism held sway. With Thatcher elected to power, the socio-economic facts quickly showed the flaws of this skewed wealth redistribution at the hands of neoliberal monetarists. For those who missed the point, so-called « maestro » Greenspan’s House Effect ended its exuberant course in the unprecedented post-WW II economic crisis known as the subprime crisis – 2007/2008 – which dotted the Is and crossed the Ts while transmuting 401K into 201K. (When you are past 45-50, you can hardly make up for such big losses even if you work like a slave for the rest of your life, hence the necessity of public Social Security, which should become the New Frontier of America and of the West.) Things are now out of control as hegemonic speculation has destroyed whole sectors of the tangible economy.

Here is the a recent « Break down of current total net worth » in the US: Bottom 50%, 2,78 %. The 50-90th %, 28,07 %. The 90-99th %, 37,32% and the Top 1 %, 32,14 %.

The top 10 % corners 69,46% ( See: «There Really Is No Middle Class Any Longer », by Tyler Durden, Tuesday, Nov 01, 2022 – 11:00 AM, Authored by Lance Roberts via The Epoch Times, https://www.zerohedge.com/markets/there-really-no-middle-class-any-longer

Here are two quick illustrations that graphically show how the various inflations are weaving themselves into an uncontrolled spiral, a process still aggravated by the continued servitude to the fallacious Marginalist and Monetarist narratives.

The CPI is here useful. It shows how Renewable sources of energy and imports, including foods etc, are inexorably making their ways into the costs of production – hence destroying the competitiveness rate of the FS which is duly registered by deteriorating trade balances: See these two graphs taken from this beautiful article: “Inflation Has Peaked”: Here’s What To Expect In Today’s CPI Report, by Tyler Durden, Wednesday, May 11, 2022 – 06:11 AM, https://www.zerohedge.com/economics/inflation-has-peaked-heres-what-expect-tomorrows-cpi-report

First graph:

Second graph with its forecasts to November 2022:

Here is the update:

The only thing that does not show up in these graph is organic inflation caused by imperfect competition etc. But the main point is the inflationary spiral and the insurance one has that fighting « inflation » in the singular just by adjusting the nominal rate to the Core inflation will simply not do.

It is interesting to see someone like prof. David Stockman taking note in his own way. See: « Stockman: Why We’ll Continue To Have High & Sticky Inflation Ahead… », by Tyler Durden, Sunday, Oct 09, 2022 – 12:30 PM, Authored by David Stockman via InternationalMan.com, https://www.zerohedge.com/economics/stockman-why-well-continue-have-high-sticky-inflation-ahead

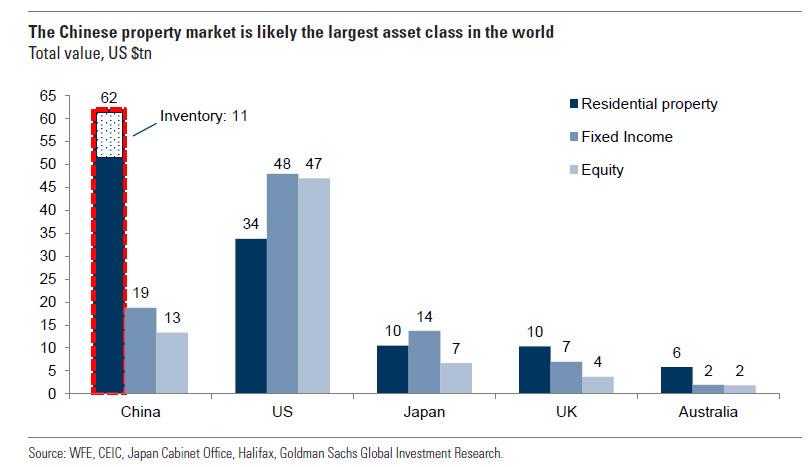

Mortgage rates naturally adjust to the FED main rate. (See : https://www.forbes.com/advisor/mortgages/mortgage-rates-history/ ) Perhaps as one tries to evaluate the evolution of the Real Estate sector and, for instance, the weight of the « rent equivalent » in it, it would be wise not to forget the dominant role played by equity funds in the US Real Estate. In China, things are not as bad as the graph below shows since China can very well nationalise the whole sector with recourse to public credit just as the New Dealers did when they established public housing. See this:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Source : « Some Good News: Rents Have Finally Peaked As Rental Market Enters “Widespread Cooldown” », by Tyler Durden, Thursday, Jan 13, 2022 – 06:00 PM, https://www.zerohedge.com/markets/finally-some-good-news-rents-have-finally-peaked-rental-market-enters-widespread-cooldown

It would seem that the FED – with a unhelpful Treasury totally entrapped into the worst neoliberal monetarist doxa – finds itself between a Hammer and a hard place. In the end, given the mountains of bonds and derivatives, including in pension funds, the FED will be enticed by the market to imitate the BoE and also preventively to fully index all new debt emission as the ECB did. Meanwhile, the Treasury, is trying to investigate new ways to help the poor speculative agents, for instance with the possibility to buyback its own T-bonds. But the 200-250 billion considered are mere trifles compared to the problem at hand. See:

(« A Treasury buyback is when the Treasury purchases previously issued Treasury debt in a secondary market transaction. The purchases can be financed out of fiscal surpluses, or by raising additional funds through debt issuance. ».

See : « Wall Street Says Treasury Buybacks Are a Long Way Off, If at All », Alexandra Harris, Thu, November 3, 2022, https://ca.finance.yahoo.com/news/wall-street-says-treasury-buybacks-135623375.html?guccounter=1&guce_referrer=aHR0cHM6Ly93d3cuYmluZy5jb20v&guce_referrer_sig=AQAAAN261LGNPG5T6dki6caxyAqEn5RQYqsji_LdjtoA2_qKDOhjkc5RqPoFlvk1zQYDds_1vaphuSPyfNEf5Ke7VQHDdBiZG2sMTFcuQNSA9t1rua4ykglbcCqe3ASABnUoGia7vQPKWJDia_cE7ISEadr5Vw6_UTOfplKKtX7hIAeh

Quotes « Alexandra Harris Thu, November 3, 2022 at 2:56 p.m.·5 min read

(Bloomberg) — The US Treasury won’t buy back government debt to shore up market functioning before May 2023, if ever, analysts are saying.» (…)

«The pledge suggests concerns on liquidity in the nearly $24 trillion Treasury market aren’t pressing for the official sector, even as liquidity metrics for the US government debt market approach crisis levels after a year of steep losses for bonds, driven by rising inflation and Federal Reserve interest-rate increases, and as the central bank simultaneously cuts some of its holdings.» (…)

« Goldman Sachs (Praveen Korapaty, William Marshall)

The likelihood that buybacks are ultimately operationalized is high, sees $200 billion to $250 billion per year in buybacks (spread across the curve) as a reasonable size for the program »

Swap lines and SDR increases

We already saw above that an emergency swap line had to be opened by the FED to the BoE.

Let us now say a final word about the mounting debt crisis in the emerging countries, which are again tragically hit by the USD carry trades just like it had happened under Volcker-Reagan. Except that today, they can count on China and the Brics +. When Volcker-Reagan raised rates to double-digit it triggered exactly what Neil Wallace had predicted in FOMC meeting, namely a « rollercoaster » (see William Greider, Secrets of the Temple,1989. See also my March 1985 analysis « The socio-economic consequences of MM. Volcker-Reagan and Co » in the Category « Another America is possible » in http://rivincitasociale.altervista.org/another-america-possible-feb-1-2017/

At this point we will only underline the recent US prospective increase of the Special Drawing Rights – SDR – of the IMF: « IMF FUNDING REQUEST: Yellen told a news conference that the Treasury has asked the U.S. Congress for permission to lend $21 billion in existing U.S. Special Drawing Rights (SDR) to IMF- Oct 14th- RTRS » in « FRA-OIS Says Powell Didn’t Pivot Yet, But Yellen Sure Did », by VBL, https://www.zerohedge.com/news/2022-10-15/fra-ois-says-powell-didnt-pivot-yellen-sure-did